(Auszug aus der Pressemitteilung)

LONDON, October 20, 2011 – PC shipments in Europe, the Middle East, and Africa (EMEA) continued to contract in 3Q11 as sustained weakness in consumer demand and increasing caution in the commercial segment led to a decline of 3.8% in overall PC shipments compared with the same quarter last year, in line with expectations. Although the mature markets in Western Europe remained the most impacted, trends across the emerging markets of Central and Eastern Europe and Middle East and Africa also noted a slowdown in demand.

PC shipments in Western Europe continued to contact for the fourth consecutive quarter, recording a decline of 10.2%, driven primarily by sustained weakness in consumer demand. On the one hand consumer spending overall has been declining due to increased caution amid the eurozone crisis and sustained high level of unemployment. On the other hand, consumers continued to allocate their disposable income in favor of media tablets and smartphones, choosing to postpone the renewal of their PCs. „In line with expectations, the Western European consumer PC market declined 20.6% in 3Q11 from a sell-in standpoint, as most channel players remained cautious with taking new orders,“ said Eszter Morvay, research manager, IDC’s EMEA Personal Computing research. „However, sell-out continued to improve, albeit moderately, indicating sustained focus on inventory depletion across several countries.“

The commercial segment in Western Europe continued to fare better and returned to soft trends, recording an increase of 3.7%. Renewals in the enterprise space, which have been driving commercial demand for the past six quarters, remained the key engine of growth this quarter. Projects that have already been in the pipeline were rolled out, while some companies may have spent the budgets allocated for this year before a potential budget freeze is imposed again as a response to the increasing economic pressure in the eurozone. In addition the third quarter is traditionally boosted by demand in the education sector, which has contributed to the positive results. However, the SMB space, particularly the small office and small business segments, continued to suffer from slow domestic demand and limited access to credit, which have been contributing to cautious spending on IT. Similarly the public administration also remained impacted by significant budget cuts, leading to weak demand for PCs.

The southern European region continued to suffer the most, with Spain and Italy contracting 37.0% and 31.3% respectively. Both countries remained constrained by very high inventory levels, which coupled with weak demand levels inhibited stronger sell-in. The economic and financial crisis has also led to a sharp drop in Greece and Portugal, which recorded a decline of 27.5% and 26.5% respectively. Among the key economies of Europe, the U.K. remained the weakest, with a 10.9% drop in shipment levels, adversely impacted not only by weak consumer demand for PCs but also sustained caution in business IT investments. However, France and Germany fared better, with a softer decline of 1.4% and 3.9% respectively, due to strong demand for commercial portables. The Nordic region displayed the strongest performance this quarter, with the four countries reaching a combined growth rate of 3.3%, thanks to strong commercial demand.

„In line with expectations, the PC markets in Central and Easter Europe [CEE] and Middle East and Africa [MEA] recorded soft growth at 4.8% and 7.4% respectively,“ said Stefania Lorenz, research director, IDC CEMA. „The CEE market saw growth across both desktop and portable form factors, with both consumer and commercial segments contributing to the positive trends. Despite the positive outcome from the overall CEE region, the Czech Republic, Poland, Slovakia, and Bulgaria performed poorly, due primarily to weak consumer sentiment in these countries. The African continent (excluding South Africa and Egypt) has outperformed the Middle East region in terms of volume growth, recording an increase of 26.4% compared with the same quarter last year, thanks to strong demand for mobility in the consumer space. The Middle East region, including South Africa and Egypt, grew 4.2%, driven by strong expansion in the portable PC market.“

Vendor Highlights

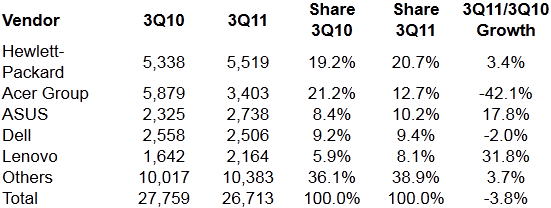

HP maintained a strong leadership and further consolidated market share in EMEA, despite the recent turmoil around the future of HP PSG. The vendor’s performance was driven by robust expansion across CEE and MEA, but shipments to Western Europe remained constrained. Weak consumer demand and focus on inventory clearance remained the key inhibitors of stronger consumer results, but HP continued to deliver outstanding performance in the commercial space, reinforcing its dominance in the segment.

Acer remained in second place despite posting yet another quarter of significant decline across all subregions. Sell-in levels continued to be adversely impacted by high inventory levels accumulated across both retail and distribution channels over the past year, and the vendor continued to focus on stock depletion. The current uncertainty around Acer’s future strategic direction as well as the alienation of many of its largest channel partners also continued to contribute to the vendor’s negative results.

ASUS moved to third place in the overall EMEA ranking, further consolidating market share by delivering strong double-digit growth in 3Q11. While the vendor’s performance was driven by robust expansion across the emerging markets, particularly the Middle East, ASUS also returned to positive trends in Western Europe. Having no issue with inventory, the vendor continued to enjoy healthy sell-in of notebooks, while increasing focus on the commercial segment.

Dell slipped to fourth place in the overall EMEA ranking, posting negative results in 3Q11. The vendor saw its PC shipments in Western Europe contract for the fourth consecutive quarter, due to a sharp drop in consumer sales, but Dell held well in the commercial segment, amid fierce competition from HP and Lenovo in the enterprise space and midmarket. The vendor also continued to deploy strong focus on the emerging markets, driving robust expansion particularly in CEE and Africa.

Lenovo maintained fifth place, enjoying robust double-digit growth and consolidating market share across each subregion. The vendor delivered outstanding performance in Western Europe, benefiting from the acquisition of Medion in the consumer space, while reinforcing its position in the commercial segment. In addition, Lenovo also continued its „Attack“ strategy, deploying strong focus on expanding across the emerging markets.

Samsung reported yet another quarter of robust growth, while Toshiba returned to positive trends, with both vendors benefiting from continued expansion across CEMA. Apple continued to enjoy the unabated momentum around the Apple brand, boosting sales particularly in the consumer space, while Sony also reported positive results, although it was constrained somewhat by an unfavorable year-on-year comparison. Fujitsu closes the ranking, posting the strongest growth among the top 10 players in 3Q11, albeit on the back of a sharp drop during the same quarter last year.

Top 5 Vendors: Europe, Middle East, and Africa (EMEA) PC Shipments*

3Q11 (Preliminary) (000 Units)

Source: IDC EMEA Quarterly PC Tracker, Preliminary Results, 3Q11, October 18, 2011

*PC shipments = desktop and notebooks.

Shipments are branded shipments for all form factors (including desktops and notebooks) and exclude x86 servers as well as OEM sales for all vendors. Data for all vendors is reported for calendar periods.

Neueste Kommentare

5. Juni 2026

31. Mai 2026

28. Mai 2026

16. Mai 2026

12. Mai 2026

29. April 2026