(Auszug aus der Pressemitteilung)

LONDON, April 20, 2009 – Following a slow down which started in the final quarter of 2008, EMEA PC shipments fell to negative trends in the first quarter of 2009 (1Q09) as anticipated. In line with forecasts, the PC market in Europe, Middle East and Africa (EMEA) displayed its first yearly decline since the 2001 recession, with sales recording –10% year-on-year growth in 1Q09, according to preliminary data released by IDC EMEA.

The CEE region remained the most affected bringing down overall EMEA results with a decline in PC shipments of –41%, while MEA slowed down as well at –6.1% growth. Western Europe held well, however, with shipments decreasing by only –0.5%, supported by sustained consumer demand and continued traction for Mini Notebooks.

“This quarter delivered an expected deceleration of the EMEA PC market as the financial crisis unfolded across the region, but while emerging markets are hit the hardest, mature economies held well considering the global environment,” said Karine Paoli, associate vice president, IDC EMEA Systems Infrastructure Solutions. “The business market is directly impacted by lower investment levels and consumer spending also slowed down since January, but the traction for Mini Notebooks helped to sustain consumer demand in Western Europe and contain overall market contraction, and will continue to do so over the coming quarters as vendors, retailers, and telco players will maintain a major push.”

Continuing to suffer from a challenging financial situation, most countries in Central Eastern Europe displayed further contraction this quarter. Russia and Ukraine remained severely constrained and several other markets declined as well. Growth in the Middle East also decelerated, but to a much lesser extent thanks to sustained demand for portable PCs.

“IDC expects the CEE region to remain strongly negative in the coming quarters, affected by the global economic downturn, which is impacting both commercial and consumer markets,“ said Stefania Lorenz, research director, Systems, IDC CEMA. “Within the CEE region, just a few countries reported positive growth, with Czech Republic and Slovakia being the most dynamic. The desktop market in the MEA region reported the lowest drop ever while notebook sales were able to remain afloat, with strong growth for portable PCs in Africa in particular.”

PC sales in Western Europe also slowed down, declining by a moderate –0.5% year on year, and slightly ahead of forecasts. Commercial sales were directly impacted by the economic downturn and declined by –14.8%, affecting both desktop and portable shipments. However, the consumer market demonstrated some resilience, despite a slowdown in consumer spending as a result of fragile consumer confidence and rising unemployment.

In Western Europe, dynamics in the portable PC market continued to be driven by consumer demand, with Mini Notebooks contributing to an impressive 28% growth despite the overall economic slowdown. The market clearly benefited from continued price declines overall, and retailers deployed aggressive deals and promotions, as cash-trapped customers were increasingly looking for a bargain and opted for low-priced entry-level systems. Continued growth of the Telco channel has also contributed to stimulate incremental demand for Mini Notebooks.

“The mini notebook momentum continued unabated in the first quarter, with shipments reaching over 2.5M, in line with IDC’s forecast,” said Eszter Morvay, research manager, IDC EMEA Personal Computing. “Whilst Acer and Asus continued to lead the Mini Notebook market, smaller vendors such as Samsung are taking advantage of this unique market opportunity to gain stronger footing in the European PC market and grab market share from traditional PC makers. On the component side, Intel and Microsoft are dominating this product segment, but the market potential in Mini Notebooks is attracting new players, who may be able to challenge them in the long-term, given they can provide unique solutions, such as all-day battery life or more user friendly interface.“

Vendor Highlights

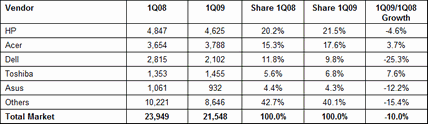

HP maintained its solid leadership in EMEA through effective strategy in both the commercial and consumer markets. Growth overall remained constrained by a slower environment and the CEE market contraction. But HP continues to drive share consolidation across the region with strong product and user marketing, and developing a closer partnership with its channel.

Acer also continued to gain share as the vendor maintained pressure in the portable PC market and a clear focus in the Mini Notebook segment, which continued to assist Acer’s performance, and offset the decline in emerging markets. The vendor also continued to benefit from desktop market consolidation in Western Europe taking share from local assemblers.

Dell faced increased challenges this quarter, directly impacted by lower business investment levels across the region, and fierce competition in the notebook space across both the commercial and consumer segments. Further expansion of its channel presence and maintained focus in the consumer space will be key to better position itself in the current environment.

Toshiba recorded another solid quarter with the strongest growth among the top 5 players, and regained the fourth position lost to Asus in 2H08. The vendor continued to benefit from a streamlined product portfolio and improved go-to-market strategy, while solid presence in the retail and SMB channel contributed to support the vendor’s performance.

Asus maintained its position in the top 5 ranking but recorded its first negative quarter, constrained primarily by the economic situation in the CEE region as the vendor continued to gain significant share in Western Europe. Asus maintained a large and solid product portfolio and continued to increase its telco presence across Europe, but faces increased competition.

Top 5 Vendors: Europe, Middle East, and Africa (EMEA) PC Shipments* 1Q09 (Preliminary)

(Unit Shipments in 000s)

Source: IDC EMEA Quarterly PC Tracker, Preliminary Results, 1Q09, April 16, 2009

Notes:

*PC shipments = desktop and notebooks.

Shipments are branded shipments for all form factors (including desktop and notebooks) and exclude x86 servers as well as OEM sales for all vendors.

Data for all vendors is reported for calendar periods.

Neueste Kommentare

8. August 2026

7. August 2026

6. August 2026

23. Juli 2026

23. Juli 2026

21. Juli 2026